B.L. Duke Launches Mobile Website

We're excited to announce our new mobile website - www.blduke.com! Our team has dedicated time and energy to create a mobile friendly website with your needs in ...

We're excited to announce our new mobile website - www.blduke.com! Our team has dedicated time and energy to create a mobile friendly website with your needs in ...

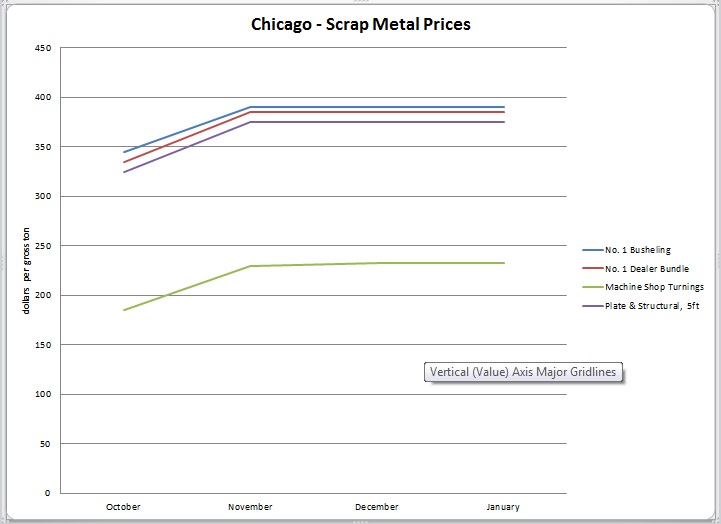

Unlike the prior three months, there is a fair amount of uncertainty regarding February's scrap market. Continuing extreme weather conditions as well as lack o ...

What can we expect to see in the scrap markets in November and throughout 2014? Hopefully something positive! From September to October 2013, we experienced rel ...

If you have been hoping that September's scrap market would heat up like the recent weather trend in the Midwest, you are going to be disappointed. At B.L. Duk ...

After what felt like an eternity of depressed scrap prices, July's pricing increase was long overdue. As we plod through the dog days of summer, the industry's ...

Be Red, White, Blue & GREEN this Fourth of July! Here are some ways we suggest being green this holiday: Recycle plastic bottles, aluminum cans, & paper ...

Finally we are beginning to hear some good news for July's Scrap Market! Most everyone in the industry believed May to be the bottom of the market and we were ...

While the U.S. steel and scrap metal market has seemed poised to move forward in recent months it has lacked the momentum needed to make any true gains. "The do ...

What are you doing to give back this holiday season? This year at B.L. Duke, we have decided to participate in a food drive to benefit the Greater Chicago Food ...

Despite the still shaky economic recovery, there’s definitely some good news out there: American manufacturing is on a steady and consistent rebound according t ...