March’s scrap market is shifting into a more balanced phase after a strong start to the year. Ferrous scrap prices held steady following two consecutive months of increases, supported by solid steel fundamentals and strong Hot Rolled Coil (HRC) pricing. In non-ferrous markets, stainless scrap firmed on higher nickel prices and tight supply, aluminum trading prices surged amid geopolitical tensions and supply disruptions in the Middle East, while copper remains elevated despite some recent volatility.

Chicago’s Ferrous Scrap Market

In Chicago, scrap prices held steady from February into March following two consecutive months of increases earlier this year, as steel mills carefully manage buying strategies and balance order books.

Export activity has slowed as rising freight rates—driven in part by conflict in the Middle East—have made overseas shipments less competitive. Despite softer export flows, strengthening steel fundamentals continue to support the domestic scrap market.

Hot Rolled Coil (HRC) prices remain a key barometer for scrap demand and are currently trading above $1,000 per short ton. The spread between HRC and Chicago No. 1 Busheling is sitting around $682 per gross ton, giving steel mills healthy operating margins and supporting continued scrap consumption. Domestic mill lead times have also extended, reflecting steady order books and mill utilization rates holding in the upper-70% range. Meanwhile, the U.S. Manufacturing PMI is hovering near the 50 expansion threshold—another signal that steel production and industrial activity remain relatively stable.

“In Chicago, strong HRC prices are still giving the mills room to buy scrap,” said Lou Plucinski. “Export has cooled off a bit, but overall it feels like a pretty balanced market.”

Overall, the Chicago market is trading in a stable range, with strong steel fundamentals offsetting slower export demand and cautious mill purchasing.

Chicago Non-Ferrous Scrap Market

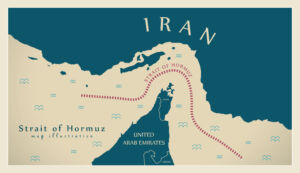

Aluminum. Aluminum markets have moved sharply higher, with trading prices rising more than 5% in recent days as tensions surrounding the conflict in Iran escalate. The move has been driven in part by supply disruptions in the Middle East, where major smelters including QATALUM and Aluminum Bahrain (ALBA) have declared force majeure on certain shipments due to gas supply constraints and shipping disruptions through the Strait of Hormuz.

While operations at the facilities remain intact, restrictions along key shipping routes have created uncertainty around near-term aluminum supply. Even short-term interruptions can tighten spot availability and increase market volatility, particularly for manufacturers relying on just-in-time deliveries. As the situation develops, the market will be watching closely to see whether shipping flows through the Strait of Hormuz stabilize or if additional supply disruptions emerge.

Stainless Steel. U.S. stainless steel scrap prices firmed during the final week of February, supported by higher nickel prices and steady demand from processors. Supply remains tight due to lingering weather-related disruptions, helping support the market.

Demand is performing well for this time of year, with finished stainless steel prices strengthening in February and expected to trade mostly sideways into March. As a result, market participants are watching movements in the nickel market closely for near-term direction.

Export demand has also become more competitive in recent weeks, placing additional pressure on domestic processors to secure material. Molybdenum-bearing grades such as 316 have seen the strongest gains, supported by firm molybdenum prices and improving export interest. This increased competition is helping establish a stronger floor for stainless scrap prices even as the broader market searches for direction.

Copper. Copper futures eased to around $5.80 per pound this week, giving back some of the previous session’s gains as the U.S. dollar strengthened and markets weighed ongoing geopolitical tensions in the Middle East. While conflict in the region has added uncertainty across commodity markets, copper traders remain focused on underlying supply and demand fundamentals.

Global copper inventories have continued to rise as elevated prices discourage physical buyers from stepping into the market. In China—the world’s largest copper consumer—demand has softened following the Lunar New Year holiday, while smelters continue to produce at record levels.

Refined copper output in China is expected to reach nearly 1.2 million tons this month, according to Shanghai Metals Market, marking a record high and contributing to growing stockpiles. The combination of rising inventories and strong production has raised questions about whether copper’s recent rally can be sustained in the near term.